Linear regression is one of the most basic yet essential tools in the arsenal of a data scientist or an engineer. Its simplicity, interpretability, and effectiveness in many applications make it a cornerstone of statistical modeling and machine learning. This article aims to provide a thorough understanding of linear regression, covering its theoretical foundations, practical applications, assumptions, implementation, and advanced techniques.

1. The Basics of Linear Regression

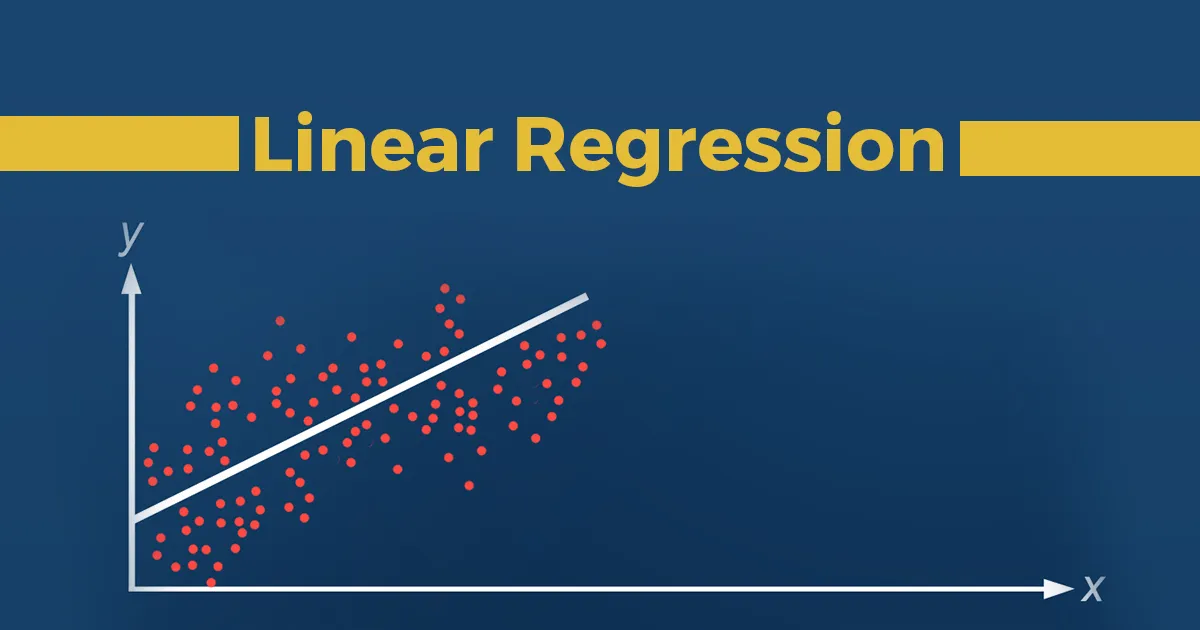

1.1 Definition

Linear regression is a statistical method for modeling the relationship between a dependent variable (also known as the response or target variable) and one or more independent variables (predictor or explanatory variables). The goal is to predict the value of the dependent variable based on the values of the independent variables.

1.2 Simple Linear Regression

In simple linear regression, there is one dependent variable, ( y ), and one independent variable, ( x ). The relationship between them can be modeled with a straight line:

y=β0+β1x

Here:

- ( y ) is the dependent variable.

- ( x ) is the independent variable.

- ( β0) is the intercept (the value of ( y ) when ( x ) is zero).

- ( β1 ) is the slope (the change in ( y ) for a one-unit change in ( x )).

1.3 Multiple Linear Regression

Multiple linear regression extends simple linear regression to include multiple independent variables:

y = β0 + β1x1 + β2x2 + ⋯ + βpxp

Here, x1,x2,…,xp are the different input variables.

3. How Linear Regression Works

2.1 The Goal

The goal of linear regression is to find the best-fitting line (or hyperplane in multiple dimensions) that minimizes the difference between the actual outcomes and the predicted outcomes. This difference is known as the error.

2.2 Ordinary Least Squares (OLS)

The most common method for finding this line is called Ordinary Least Squares (OLS). It works by minimizing the sum of the squared differences (errors) between the observed and predicted outcomes.

Cost(β)= ∑i=1n(yi−y^i)2

- yi is the actual outcome.

- y^i is the predicted outcome.

3. Theoretical Foundations

3.1 Least Squares Estimation

The most common method for estimating the coefficients in linear regression is the Ordinary Least Squares (OLS) method. OLS aims to find the line (or hyperplane in multiple dimensions) that minimizes the sum of the squared differences between the observed and predicted values of the dependent variable. Mathematically, the objective is to minimize the cost function:

Cost(β)=∑i=1n(yi−y^i)2

Where:

- yi is the observed value.

- ^i is the predicted value, y^i=β0+β1xi1+β2xi2+⋯+βpxipy^i=β0+β1xi1+β2xi2+⋯+βpxip.

- n is the number of observations.

3.2 Matrix Representation

Linear regression can also be represented using matrix notation, which simplifies the calculations, especially for multiple linear regression. Let ( \mathbf{X} ) be the matrix of input features (including a column of ones for the intercept), ( \mathbf{y} ) be the vector of target values, and ( \mathbf{\beta} ) be the vector of coefficients. The linear regression model can be written as:

y=Xβ+ϵ

The OLS estimator for β is given by:

β^=(X⊤X)−1X⊤y

3.3 Assumptions of Linear Regression

Linear regression relies on several key assumptions to ensure the validity and accuracy of the model:

- Linearity: The relationship between the independent and dependent variables is linear.

- Independence: Observations are independent of each other.

- Homoscedasticity: The variance of the error terms is constant across all levels of the independent variables.

- Normality: The error terms are normally distributed (especially important for hypothesis testing).

- No Multicollinearity: The independent variables are not highly correlated with each other.

4. Practical Applications

Linear regression has a wide range of applications across various fields due to its simplicity and effectiveness. Here are some common use cases:

4.1 Predictive Modeling

Linear regression is often used for predictive modeling, where the goal is to predict future values based on historical data. For example, it can be used to forecast sales, stock prices, or demand for products.

4.2 Econometrics

In economics, linear regression is used to model relationships between economic variables, such as the impact of interest rates on investment or the effect of education on income.

4.3 Engineering

Engineers use linear regression to model and predict outcomes in various processes, such as estimating the strength of materials based on their composition or predicting system failures based on operational data.

4.4 Healthcare

In healthcare, linear regression can be used to predict patient outcomes based on medical history and demographic factors, such as predicting the risk of developing a disease.

5. Implementation

Implementing linear regression is straightforward, thanks to various statistical and machine learning libraries available in programming languages like Python and R. Here, we will focus on implementing linear regression using Python’s Scikit-Learn library.

5.1 Data Preparation

Before implementing linear regression, it is crucial to prepare the data, which involves cleaning, transforming, and splitting the data into training and testing sets.

import pandas as pd

from sklearn.model_selection import train_test_split

# Load dataset

data = pd.read_csv('data.csv')

# Select features and target

X = data[['feature1', 'feature2', 'feature3']]

y = data['target']

# Split data into training and testing sets

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.2, random_state=42)5.2 Training the Model

After preparing the data, we can train the linear regression model using Scikit-Learn.

from sklearn.linear_model import LinearRegression

# Create a linear regression model

model = LinearRegression()

# Train the model

model.fit(X_train, y_train)5.3 Making Predictions

Once the model is trained, we can use it to make predictions on the testing set.

# Make predictions on the testing set

y_pred = model.predict(X_test)5.4 Evaluating the Model

Evaluating the performance of the linear regression model is crucial to ensure its accuracy and reliability. Common evaluation metrics include Mean Absolute Error (MAE), Mean Squared Error (MSE), and R-squared ((R^2)).

from sklearn.metrics import mean_absolute_error, mean_squared_error, r2_score

# Calculate evaluation metrics

mae = mean_absolute_error(y_test, y_pred)

mse = mean_squared_error(y_test, y_pred)

r2 = r2_score(y_test, y_pred)

print(f'MAE: {mae}')

print(f'MSE: {mse}')

print(f'R-squared: {r2}')6. Advanced Techniques

While basic linear regression is powerful, there are several advanced techniques and extensions that can enhance its capabilities and address its limitations.

6.1 Polynomial Regression

Polynomial regression is an extension of linear regression that models the relationship between the independent and dependent variables as an nth degree polynomial.

from sklearn.preprocessing import PolynomialFeatures

# Create polynomial features

poly = PolynomialFeatures(degree=2)

X_poly = poly.fit_transform(X)

# Train the model with polynomial features

model.fit(X_poly, y)6.2 Ridge and Lasso Regression

Ridge and Lasso regression are regularization techniques that add a penalty term to the cost function to prevent overfitting and improve model generalization.

- Ridge Regression: Adds the L2 penalty term.

[ \text{Cost}(\beta) = \sum_{i=1}^n (y_i – \hat{y}i)^2 + \lambda \sum{j=1}^p \beta_j^2 ]

- Lasso Regression: Adds the L1 penalty term.

[ \text{Cost}(\beta) = \sum_{i=1}^n (y_i – \hat{y}i)^2 + \lambda \sum{j=1}^p |\beta_j| ]

from sklearn.linear_model import Ridge, Lasso

# Create Ridge and Lasso models

ridge_model = Ridge(alpha=1.0)

lasso_model = Lasso(alpha=1.0)

# Train the models

ridge_model.fit(X_train, y_train)

lasso_model.fit(X_train, y_train)6.3 Handling Multicollinearity

Multicollinearity occurs when independent variables are highly correlated, which can distort the estimates of the coefficients. Techniques to handle multicollinearity include:

- Removing highly correlated predictors.

- Principal Component Analysis (PCA): A dimensionality reduction technique that transforms the features into a set of orthogonal components.

from sklearn.decomposition import PCA

# Apply PCA

pca = PCA(n_components=2)

X_pca = pca.fit_transform(X)

# Train the model with PCA features

model.fit(X_pca, y)7. Assumptions Diagnostics and Remediation

Diagnosing and addressing the violations of the assumptions of linear regression is crucial for building reliable models.

7.1 Linearity

Check the linearity assumption by plotting the observed vs. predicted values. If the plot shows a linear relationship, the assumption holds.

7.2 Independence

Check the independence assumption by plotting the residuals (errors) against the order of the observations. If the residuals appear randomly scattered, the assumption holds.

7.3 Homoscedasticity

Check homoscedasticity by plotting the residuals against the predicted values. If the variance of the residuals is constant, the assumption holds. If the plot shows a pattern, consider transforming the dependent variable or using weighted least squares.

7.4 Normality

Check the normality assumption by plotting a histogram or Q-Q plot of the residuals. If the residuals are normally distributed, the assumption holds. If not, consider applying a transformation to the dependent variable (e.g., log or square root transformation).

7.5 Multicollinearity

Check multicollinearity by calculating the Variance Inflation Factor (VIF) for each predictor. A VIF value greater than 10 indicates high multicollinearity.

from statsmodels.stats.outliers_influence import variance_inflation_factor

# Calculate VIF

vif = pd.DataFrame()

vif['Feature'] = X.columns

vif['VIF'] = [variance_inflation_factor(X.values, i) for i in range(X.shape[1])]

print(vif)Conclusion

Linear regression is a powerful and versatile tool for modeling and predicting continuous outcomes based on one or more predictor variables. Understanding its theoretical foundations, assumptions, and practical implementation is essential for building reliable and interpretable models. By mastering both basic and advanced techniques, engineers and data scientists can leverage linear regression to solve a wide range of real-world problems.

References

- Hastie, T., Tibshirani, R., & Friedman, J. (2009). The Elements of Statistical Learning: Data Mining, Inference, and Prediction. Springer.

- James, G., Witten, D., Hastie, T., & Tibshirani, R. (2013). An Introduction to Statistical Learning: With Applications in R. Springer.

- Pedregosa, F., Varoquaux, G., Gramfort, A., Michel, V., Thirion, B., Grisel, O., … & Duchesnay, É. (2011). Scikit-learn: Machine Learning in Python. Journal of Machine Learning Research, 12, 2825-2830.

- Kutner, M. H., Nachtsheim, C. J., Neter, J., & Li, W. (2004). Applied Linear Statistical Models. McGraw-Hill Irwin.

- Montgomery, D. C., Peck, E. A., & Vining, G. G. (2012). Introduction to Linear Regression Analysis. Wiley.

This comprehensive article provides a detailed overview of linear regression, from its basic principles to advanced techniques, ensuring that engineers and data scientists can effectively use this fundamental algorithm in their work.

Leave a Reply